1. Stop disadvantages for part-time employees

Companies can reduce or completely abolish the coordination deduction in their occupational retirement provision. This deduction occurs in the calculation of the amount of monthly savings contributions. If the deduction is the same for all employees – regardless of their working hours – it is particularly significant for part-time employees, as it disproportionately reduces the amount of their savings.

2. Offer more than the mandatory

Companies have the possibility to pay savings contributions that are generally higher than the statutory minimum. This allows them to create flexibility in two senses: On the one hand, in the case of extra-mandatory benefits, it is more likely that a temporary reduction in working hours becomes possible without resulting in a problematic shortfall. On the other hand, it opens up the likelihood that employees also pay in more. This is because the law requires a company to pay at least half of the savings contributions. If employees are given the opportunity to make so-called voluntary purchases, they can close any past shortfalls during periods of higher income. It is also important for companies to regularly communicate such offers to employees – those who do good should not forget to talk about it.

3. Save from as early as 18

Companies can optimize the savings process and offer employees the opportunity to save for their pension from the age of 18, even though it is only mandatory from the age of 24. If employees start saving earlier, they either receive a higher pension later or can reduce the percentages in the meantime without this having too much of an impact.

4. Introduce optional savings plans

Companies can offer what are called optional savings plans: An optional savings plan is comprised of two additional savings plans that the company can offer to employees. This not only encourages your employees to make additional savings, but also offers them a larger scope when it comes to shaping their retirement provision.

5. Attracting men to part-time work

Finally, companies can generally position themselves as modern employers and also enable men to work part-time. This can prevent women from having to give up their job or greatly reduce their workload immediately after giving birth. This keeps valuable know-how within the company, and the amount of savings for retirement provision is more evenly balanced between genders.

6. Do good and talk about it

If companies make such offers, they should also talk about them, of course, and show their employees what the employer is doing for their future, as well as what the employees themselves can do to ensure their financial security after retirement. Getting to grips with the Swiss pension system and investment mechanisms in general helps them to improve their financial literacy and gain confidence in their own expertise. It is best for employers to address the issue of retirement provision during the employment interview and also provide regular information afterwards.

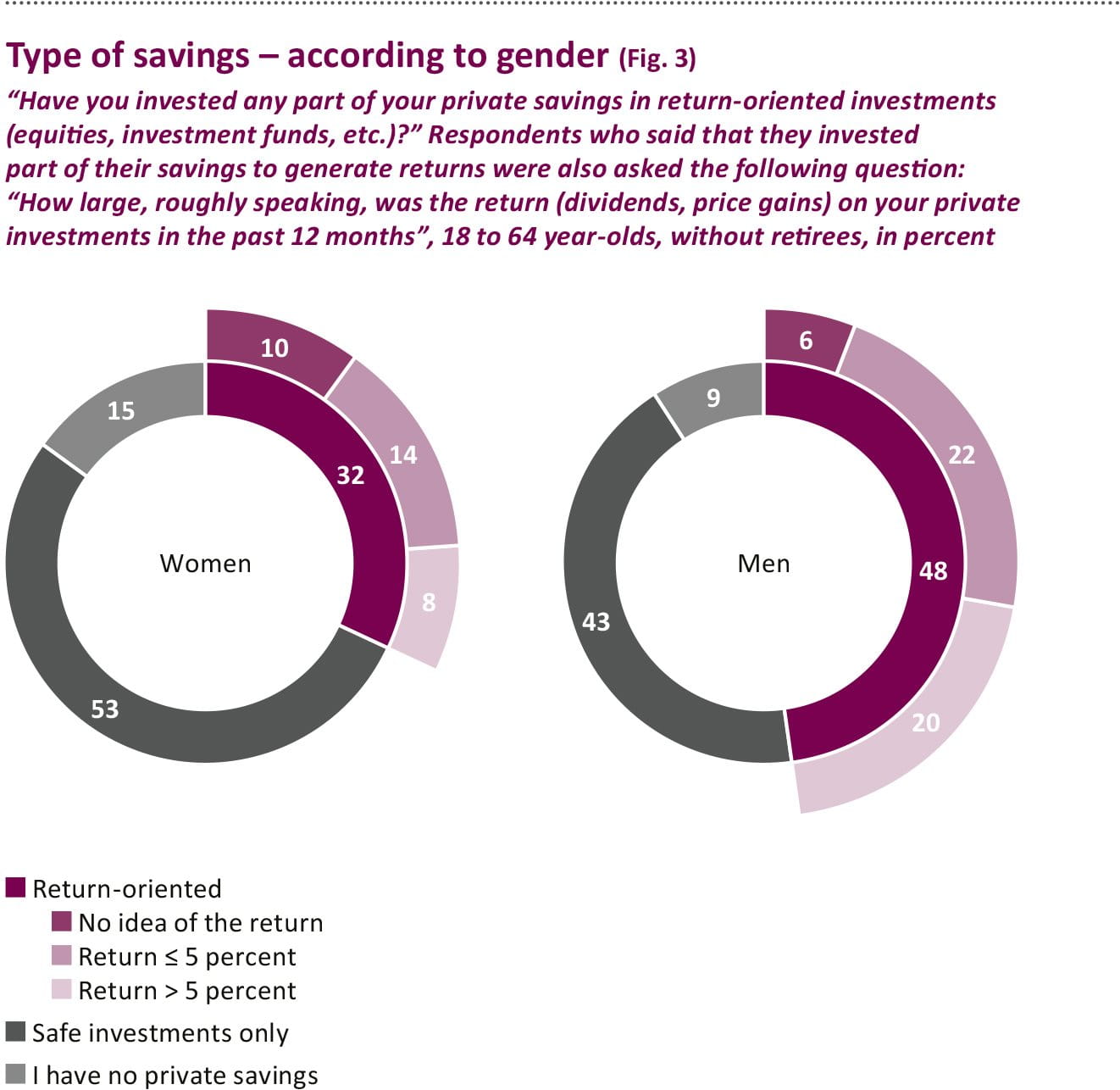

Women in particular can benefit from this information: Those interviewed for the study stated they lack the necessary investment expertise far more frequently than men, which is probably why women are more inclined to invest their savings conservatively. While as many as 48 percent of men invest their savings with a focus on returns, the figure for women is only 32 percent. Women are therefore more likely to opt for financial products that focus on preserving the value of their savings.