It pays to be well informed about occupational retirement provision

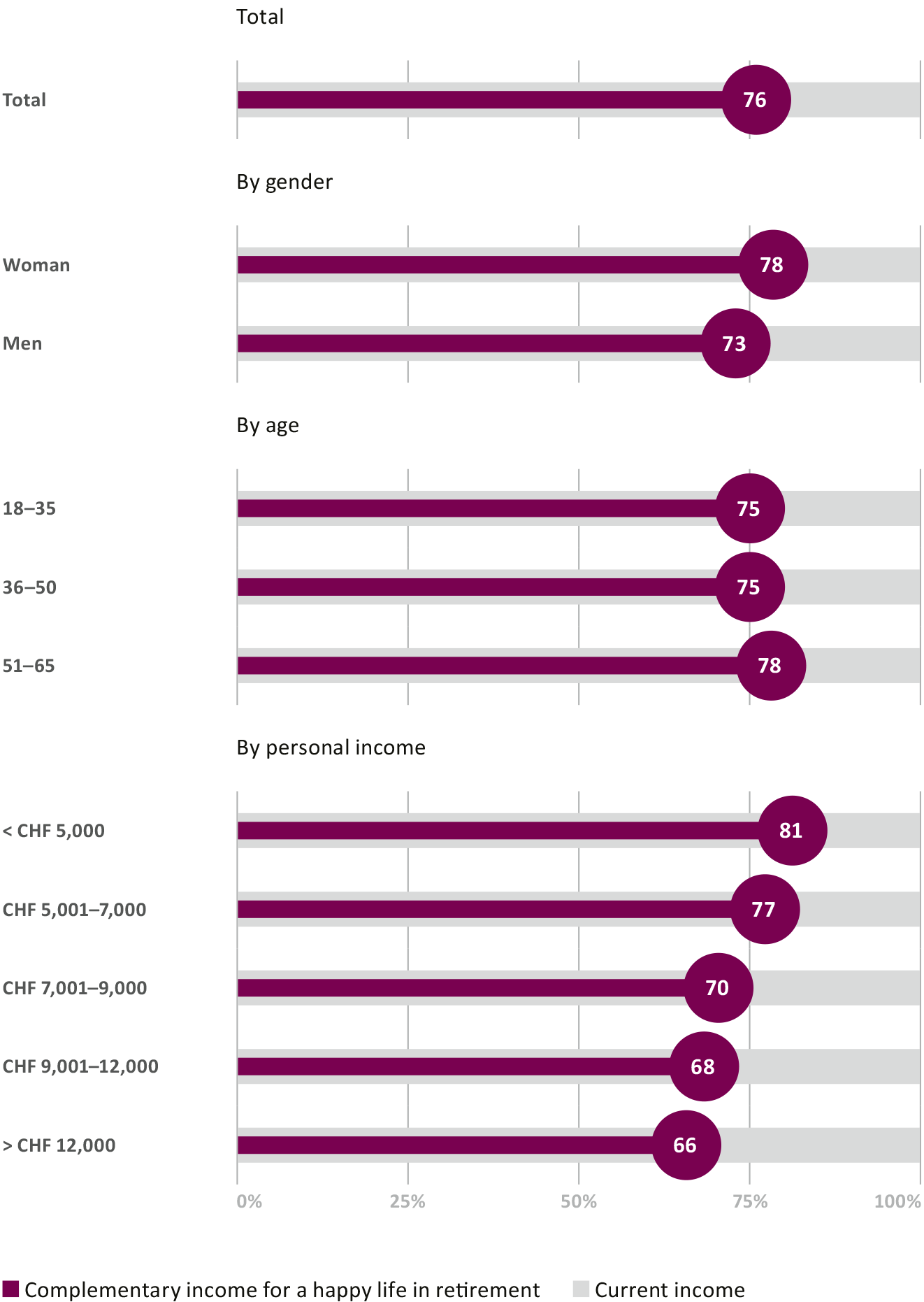

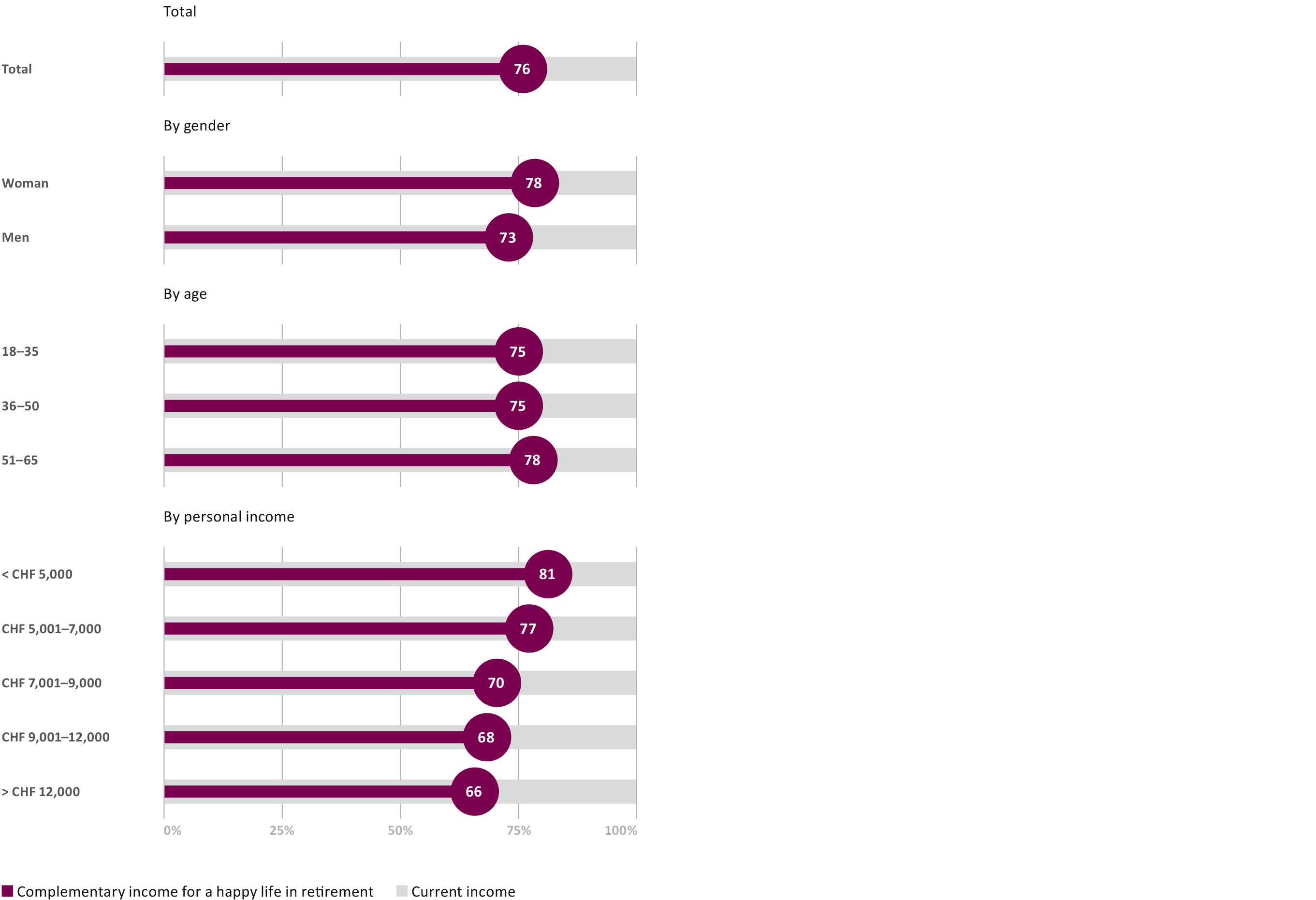

How can we ensure that the 2nd pillar stays fit for its purpose in future? There has been intense discussion on this topic. Nevertheless, many people are unaware of the important role that occupational retirement provision plays for their personal retirement provision. The current study from the series "Fair play in occupational retirement provision" illustrates the consequences of this lack of understanding – the gap between dream and reality when it comes to retirement income is getting bigger. What does this mean for employers? They are responsible for educating their employees about this topic.